Calculate the Present Value of 100 in 6 Years Using 6 4 Interest Rate With Continuous Compounding

Lesson 9: Frequency of Compounding

This lesson discusses the frequency of compounding and its affect on the present and future values using the compound interest functions presented in Assessors' Handbook Section 505 (AH 505), Capitalization Formulas and Tables. The lesson:

- Explains compounding frequency and intra-year compounding,

- Demonstrated calculation of FW$1 and PW$1 factors given monthly compounding, and

- Concludes with generalizations with respect to frequency of compounding and future and present value.

Intra-Year Compounding

Up to this point, we generally have assumed that interest was calculated at the end of each year, based on the principal balance at the beginning of the year and the annual interest rate. That is, we have assumed that interest was compounded (or discounted) on an annual basis, and in solving problems we have used the annual compounding pages in AH 505.

Compounding interest more than once a year is called "intra-year compounding". Interest may be compounded on a semi-annual, quarterly, monthly, daily, or even continuous basis. When interest is compounded more than once a year, this affects both future and present-value calculations.

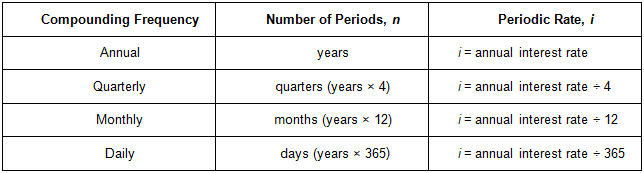

With intra-year compounding, the periodic interest rate, instead of being the stated annual rate, becomes the stated annual rate divided by the number of compounding periods per year. The number of periods, instead of being the number of years, becomes the number of compounding periods per year multiplied by the number of years.

As shown in the following table:

With monthly compounding, for example, the stated annual interest rate is divided by 12 to find the periodic (monthly) rate, and the number of years is multiplied by 12 to determine the number of (monthly) periods.

Calculating a FW$1 Factor Given Monthly Compounding

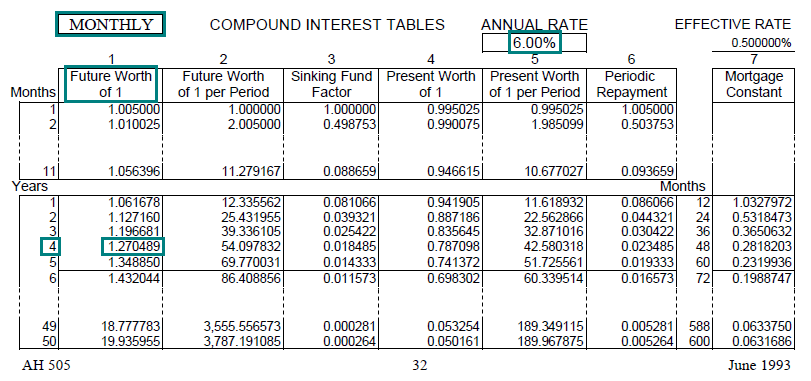

In lesson 2, we calculated the annual FW$1 factor at a stated annual rate of 6% for 4 years with annual compounding. The resulting factor was 1.262477.

Now let's calculate the FW$1 for an annual rate of 6% for 4 years, but with monthly compounding. In this case, the periodic monthly rate is 0.5% (one-half of one percent per month, 6% ÷ 12), and the number of monthly compounding periods is 48 (12 periods/year × 4 years).

In order to calculate the FW$1 factor for 4 years at an annual interest rate of 6%, with monthly compounding, use the formula below:

- FW$1 = (1 + i)n

- FW$1 = (1 + 0.5%)48

- FW$1 = (1 + 0.005)48

- FW$1 = (1.005)48

- FW$1 = 1.270489

The FW$1 factor with monthly compounding, 1.270489, is slightly greater than the factor with annual compounding, 1.262477. If we had invested $100 at an annual rate of 6% with monthly compounding we would have ended up with $127.05 four years later; with annual compounding we would have ended up with $126.25.

AH 505 contains separate sets of compound interest factors for annual and monthly compounding. Factors for annual compounding are on the odd-numbered pages; factors for monthly compounding are on the even-numbered pages.The FW$1 factor for 4 years at an annual interest rate of 6%, with monthly compounding, is in AH 505, page 32 (monthly page).

Link to AH 505, page 32

Calculating a PW$1 Factor Given Monthly Compounding

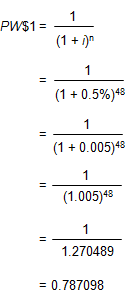

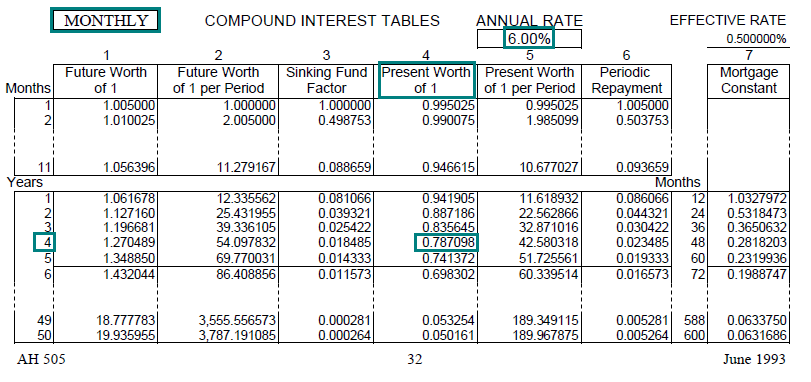

In lesson 3, we calculated the PW$1 factor at an annual rate of 6% for 4 years with annual compounding. The resulting factor was 0.792094.

Let's calculate the PW$1 factor for 4 years at an annual interest rate of 6%, with monthly compounding. In this case, the periodic monthly rate is 0.5% (one-half of one percent per month, 6% ÷ 12), and the number of monthly compounding periods is 48 (12 periods/year × 4 years).

In order to calculate the PW$1 factor for 4 years at an annual interest rate of 6%, with monthly compounding, use the formula below:

The PW$1 factor for 4 years at an annual interest rate of 6%, with monthly compounding, can be found in AH 505, page 32. The amount of the factor is 0.787098.

Link to AH 505, page 32

Generalizations

The following two generalizations can be made with respect to frequency of compounding and future and present values:

- When interest is compounded more than once a year, a future value will always be higher than it would have been with annual compounding, all else being equal.

- When interest is compounded more than once a year, a present value will always be lower than it would have been with annual compounding, all else being equal.

Thus, with our examples for the FW$1 and the PW$1:

- Given FW$1, at a rate of 6%, for a term of 4 years: 1.270489 (compounded monthly) > 1.262477 (compounded annually)

- Given PW$1, at a rate of 6%, for a term of 4 years: 0.787098 (compounded monthly < 0.792094 (compounded annually)

We would have obtained similar results with FW$1/P and PW$1/P, respectively.

Most appraisal problems involve annual payments and require the use of annual factors. Monthly factors are also useful because most mortgage loans are based on monthly payments, and it is often necessary to make mortgage calculations as part of an appraisal problem.

For other compounding periods, the factors for which are not included in AH 505, the appraiser can calculate the desired factor from the appropriate compound interest formula. As noted, AH 505 contains factors for annual and monthly compounding only.

Source: https://www.boe.ca.gov/info/tvm/lesson9.html

0 Response to "Calculate the Present Value of 100 in 6 Years Using 6 4 Interest Rate With Continuous Compounding"

Post a Comment